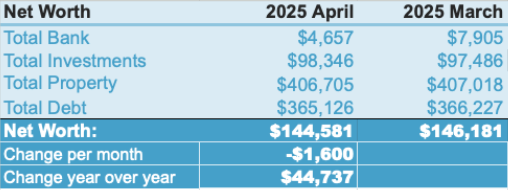

Starting Net Worth: $146,181

April brought one of the most dramatic storylines of 2025 so far. The stock market went through what many investors nicknamed the “tariff tantrum,” a quick but intense pullback sparked by concerns surrounding new trade policies. What made this episode especially interesting was how quickly things reversed. If you had gone to sleep on March 31st and woken up on May 1st, you might not have realized anything happened at all, because the market ultimately settled close to where it started. The path to get there, however, was anything but calm. For long term investors, episodes like this are powerful reminders that short term volatility and long term results are not the same thing. Sharp swings happen, but they do not automatically change the broader trajectory of the market or an investor’s long term plan.

During this period of heightened volatility, we decided to make a few intentional adjustments. First, we added extra money to our brokerage account so we could purchase additional shares at lower prices. Declines can be uncomfortable, but they also represent opportunities to buy the same investments at a discount. This approach aligns with one of our guiding principles: focus on accumulating shares over time and let the market reward patience.

We also revisited the investment strategy in our retirement accounts. After previously reducing our exposure, we increased the risk level back to what we call double exposure. In practical terms, this means we are once again embracing a higher degree of risk within our retirement savings. We feel comfortable doing this because these accounts will not be touched for more than thirty years. With such a long time horizon, short term market movements matter far less than the compounding potential that can come from taking on greater risk. Double exposure is highly volatile and is not something I recommend for everyone. It is a strategy that should be discussed with a financial professional before being used in your investments. Even with the increased exposure, we remain grounded in broad index based investing. The core philosophy stays the same: avoid chasing individual winners and instead invest in diversified, low cost indexes. The primary change is the use of leveraged index exposure within the retirement accounts, which is a way of increasing long term growth potential while keeping the underlying investment style consistent.

April’s roller coaster reinforced the importance of staying focused on long term goals rather than getting swept up in the noise of short term market reactions. By staying disciplined and intentional, even turbulent months can become opportunities rather than setbacks.

Ending Net Worth: $144,581

None of the above information is a recommendation. This blog is purely intended as commentary on things that have happened along our financial journey.